Steel prices have been in a tangled and volatile trend recently. This week, hot metal production edged down slightly but remained at a high level. According to the SMM survey, four blast furnaces are scheduled for maintenance next week, while another four plan to resume production. In the short term, there is still room for hot metal production to decline.

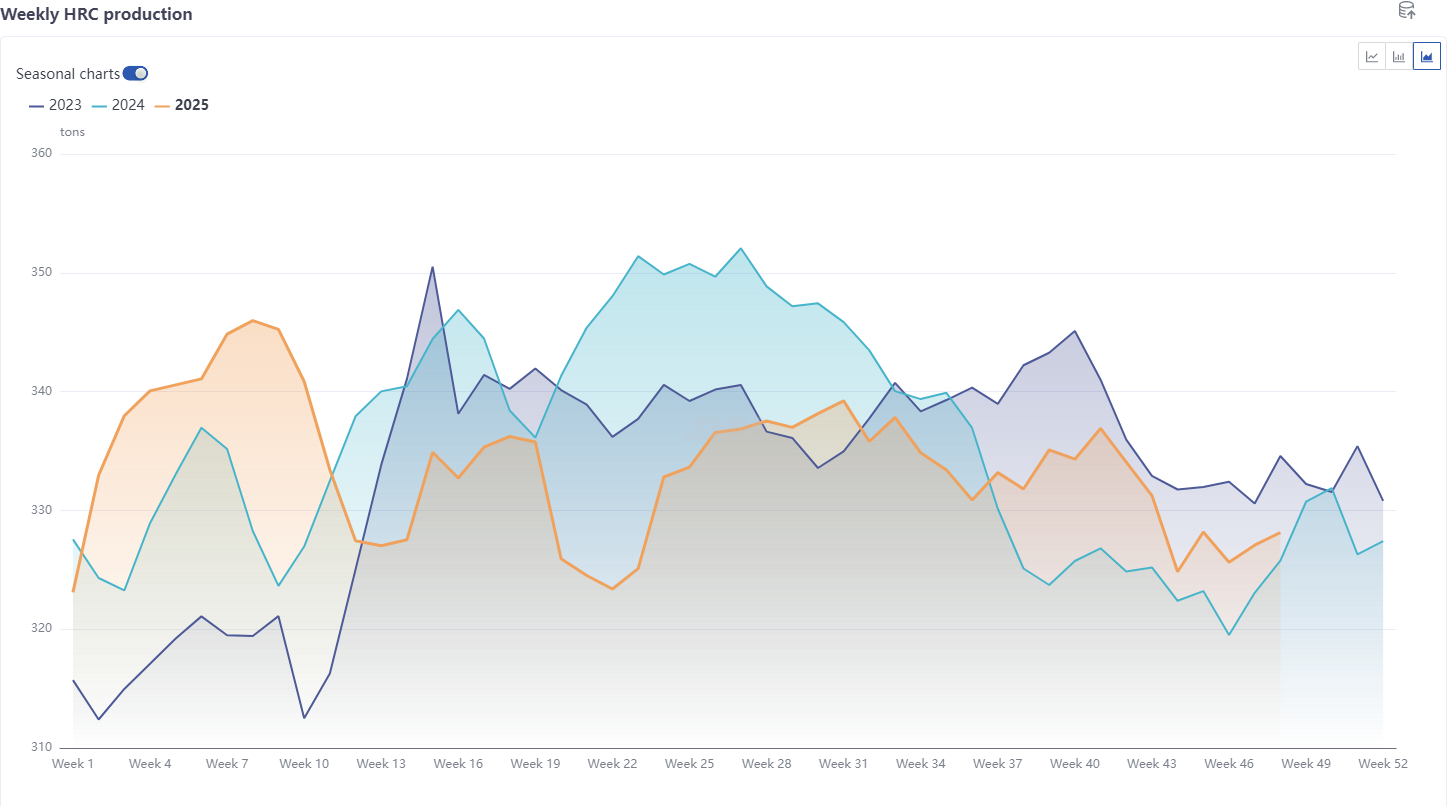

Finished products, supply side, influenced by maintenance and profit factors: rebar production averaged 2.055 million mt, down 0.27% MoM and 12.11% YoY, showing a MoM decrease and significantly lower than the same period in previous years; hot-rolled coil production averaged 3.2696 million mt, down 1.45% MoM and up 1.56% YoY, indicating a MoM decrease and higher than the same period in previous years.

Overall, rebar production remained low, while the supply of sheets & plates, especially hot-rolled coils, stayed at relatively high levels for the same period.

Demand side, the average apparent consumption of rebar in November was 2.2189 million mt, up 7.72% MoM but down 4.03% YoY, showing a MoM increase but a YoY decline compared to the same period in previous years. The average apparent consumption of hot-rolled coils was 3.3401 million mt, up 6.72% MoM but down 1.16% YoY, indicating a MoM rebound but a slight YoY drop. Overall, rebar demand was weak. For sheets & plates, in November, the home appliance sector in manufacturing was more affected by the off-season, while the automotive industry remained relatively stable. Market shipments were relatively poor, but steel mills' order intake for specialty steel was moderate. Overall, demand for sheets & plates pulled back slightly but still demonstrated strong resilience.

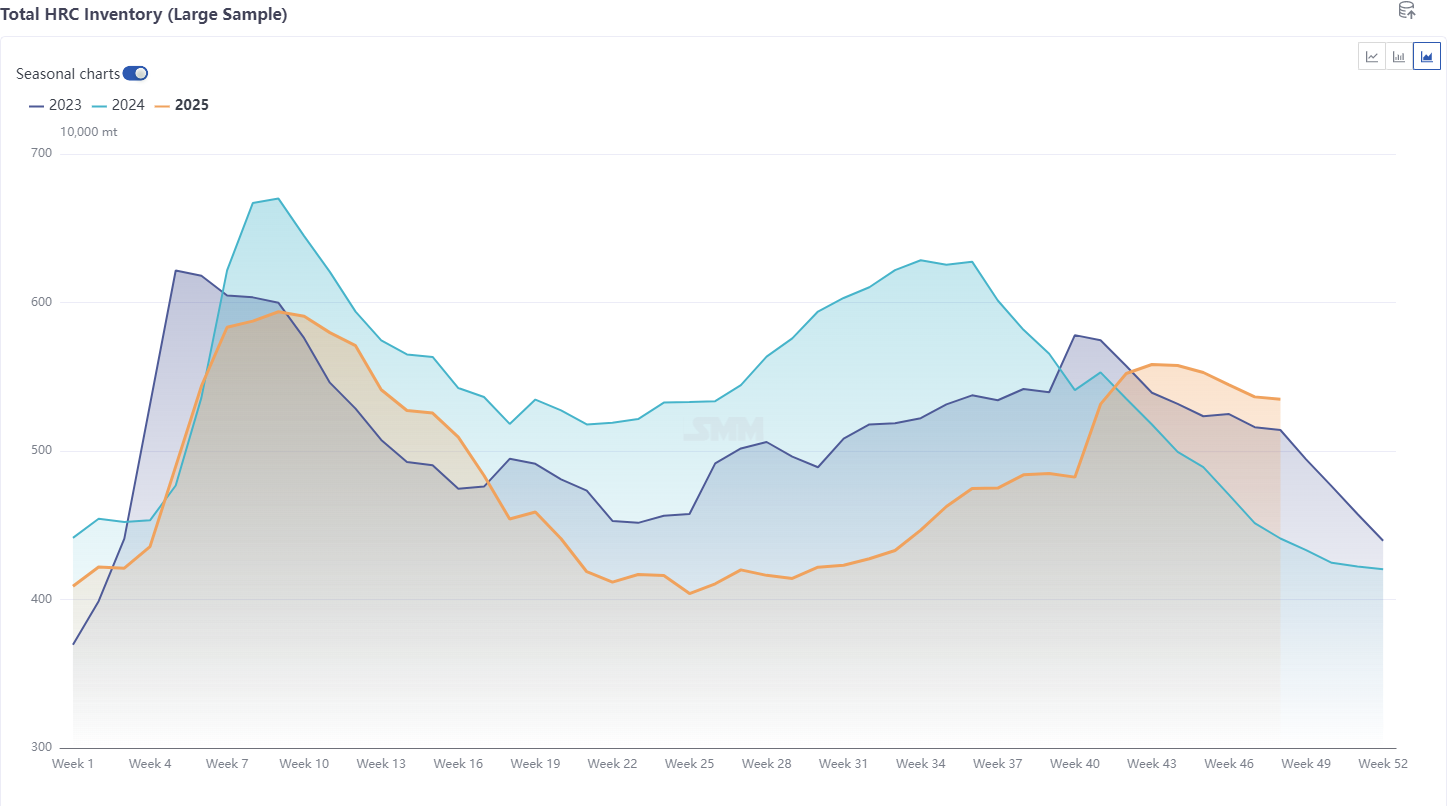

Inventory, rebar inventory up 24% YoY, HRC inventory up 28% YoY, overall inventory of the five major steel products higher than last year, sheets & plates inventory trend significantly different from 2021-2024, destocking pace relatively slow. According to the latest SMM data: this week, SMM statistics show national social inventory of HRC in 86 warehouses (large sample) at 4.2565 million mt, up 21,500 mt WoW, up 0.51% WoW, up 34.4% YoY on a Gregorian calendar basis. National social inventory increased this week. By region, although east China, south China, and north-east China continued destocking, due to large increases in north China and central China, overall inventory showed buildup. On one hand, arrival supply pressure increased, but demand could not match and digest well; on the other hand, environmental protection transport capacity shortages in some northern markets led to sheets & plates inventory accumulation. However, from the overall perspective of the five major steel products, inventory is still in destocking.

Overall, from the fundamental perspective of steel, steel prices are constrained above by weak actual demand, while below, they are supported by costs and, once prices fall to a certain level, bolstered by exports.

Considering the impact of steel mill maintenance, profits, and seasonal weakening in demand, rebar supply-demand is projected to decline further in December. For hot-rolled coil, the currently disclosed impact from maintenance is estimated to increase by around 170,000–250,000 mt MoM from November, with maintenance concentrated in mills in northern and east China. HRC production in December is unlikely to see significant growth, with limited fluctuation room MoM from November. On the demand side, year-end manufacturing typically sees some carry-over effects. By segment, policy adjustments in the automotive industry are expected to continue stimulating demand release. For home appliances, the latest production schedule for the three major white goods shows a 14% decline compared to last year, due to both the high base effect from the previous year and weakening actual demand after policy support faded. Overall, demand for cold-rolled and hot-rolled coils in December has limited upside room but also limited downside room.

Therefore, steel inventories are projected to continue declining in December, but the pace of destocking may be less than ideal, especially for sheets & plates, which are expected to maintain a slow destocking pace.

From a fundamental perspective, the steel supply-demand pattern is not expected to show significant changes MoM from November. Inventory continues to decline, and the risk of a sharp price drop remains low. Moreover, under the influence of declining profits, maintenance impacts, or environmental protection policies, the probability of easing supply pressure may increase.

Entering December, the impact of fundamentals has weakened, while macro influences have intensified. The macro focus in December centers on two important domestic meetings. As the inaugural year of the "16th Five-Year Plan," the market is highly attentive to whether there will be new policies aimed at stabilizing the real estate sector, expanding domestic demand, and promoting anti-involution. Attention is also on the expectations gap regarding policies. Before the meetings convene, there is room for buying on dips.

Conclusion: The supply-demand imbalance has accumulated to a relatively limited extent, with relatively small room for further deterioration MoM from November. In the short term, focus on the most-traded hot-rolled coil futures contract at 3,230–3,330. In December, coupled with rising macro expectations, steel prices may have room to rise before the meeting, but the upside is likely to be limited, mainly due to persistent destocking pressure for sheets & plates and relatively weak sales performance in the market, which may also constrain a smooth price increase.

![[SMM Hot-Rolled Arrivals] Arrivals in Major Mainstream Markets Pulled Back in the First Week After the Holiday](https://imgqn.smm.cn/usercenter/QMaot20251217171719.jpg)